Zero-down solar programs have revolutionized renewable energy accessibility, enabling homeowners to install solar panels without upfront costs while immediately reducing monthly electricity expenses. Through innovative financing mechanisms like Power Purchase Agreements (PPAs) and solar leases, these programs eliminate the traditional financial barriers to solar adoption, making clean energy attainable for a broader demographic of homeowners.

By leveraging federal tax incentives, state-level rebates, and competitive financing options, zero-down solar installations have emerged as a compelling solution for sustainable home energy management. These programs typically include comprehensive coverage for installation, maintenance, and monitoring services, ensuring optimal system performance while protecting homeowners from unexpected costs.

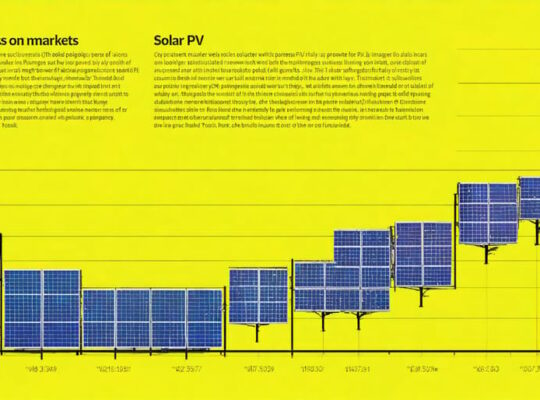

Recent market analysis indicates that zero-down solar programs have contributed significantly to the 40% annual growth in residential solar installations, with participating households reporting average energy savings of 20-30% on their monthly utility bills. This financing model has become particularly attractive as improved solar technology efficiency and decreased equipment costs continue to enhance the overall value proposition for homeowners seeking energy independence.

The rise of these programs represents a critical intersection of environmental responsibility and financial pragmatism, offering a practical pathway for households to transition to renewable energy while maintaining fiscal stability.

Understanding Zero Down Solar Financing

Solar Loans vs. Solar Leases vs. Power Purchase Agreements

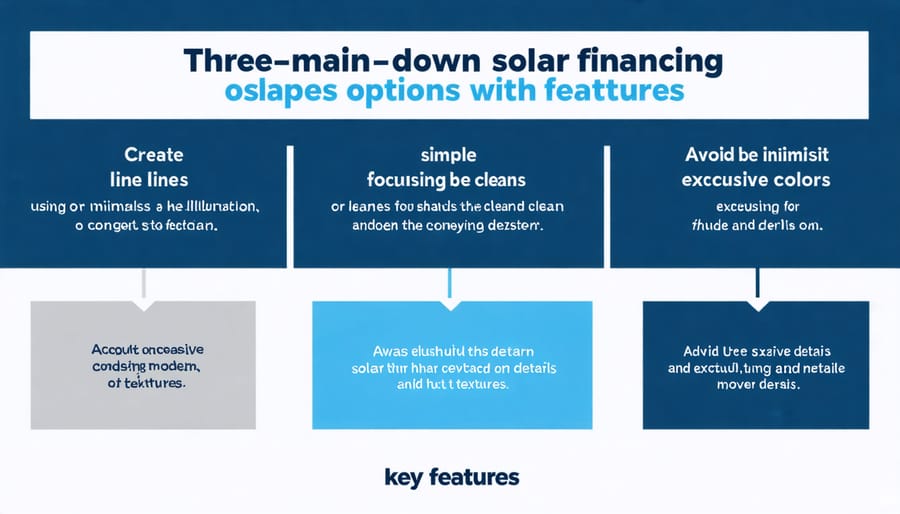

When exploring solar financing options, homeowners typically encounter three primary pathways: solar loans, solar leases, and power purchase agreements (PPAs). Each option offers distinct advantages and considerations for achieving zero-down solar installation.

Solar loans allow homeowners to maintain system ownership while spreading costs over time. With this option, property owners benefit from tax incentives, increased property value, and complete control over their solar installation. Monthly loan payments typically remain fixed, providing predictable expenses throughout the loan term.

Solar leases enable homeowners to use solar equipment without ownership responsibilities. The leasing company maintains and insures the system, while homeowners pay a fixed monthly lease payment. This arrangement often includes performance guarantees but may not qualify for certain tax incentives.

PPAs function similarly to leases but with payment based on actual energy production. Homeowners purchase solar electricity at a predetermined rate, usually lower than utility prices, with minimal responsibility for system maintenance. While PPAs offer immediate savings, rate escalators may increase payments over time.

Each financing mechanism presents unique advantages depending on financial goals, tax situation, and long-term ownership preferences. Understanding these distinctions enables informed decision-making aligned with individual circumstances and energy objectives.

Qualifying Criteria for Zero Down Programs

To qualify for zero down solar programs, homeowners must meet specific criteria established by financing providers and local regulations. Primary requirements typically include a minimum credit score of 650, though some programs may accept scores as low as 600. Homeowners must demonstrate stable employment history and sufficient income to cover potential monthly payments.

Property requirements are equally important. The home must be owner-occupied and have a clear title. The roof should be in good condition with at least 10-15 years of remaining life, and the property must receive adequate sunlight exposure for optimal solar panel performance. Most programs require homeowners to have a reliable payment history with their current utility provider.

Additionally, participants must be located within eligible service territories and comply with local zoning regulations and HOA requirements, if applicable. Some programs may require homeowners to maintain specific debt-to-income ratios, typically below 45%. Insurance coverage for the solar installation is often mandatory, and homeowners must agree to system maintenance terms outlined in the program agreement.

Financial Benefits and Savings Analysis

Long-term Cost Savings Breakdown

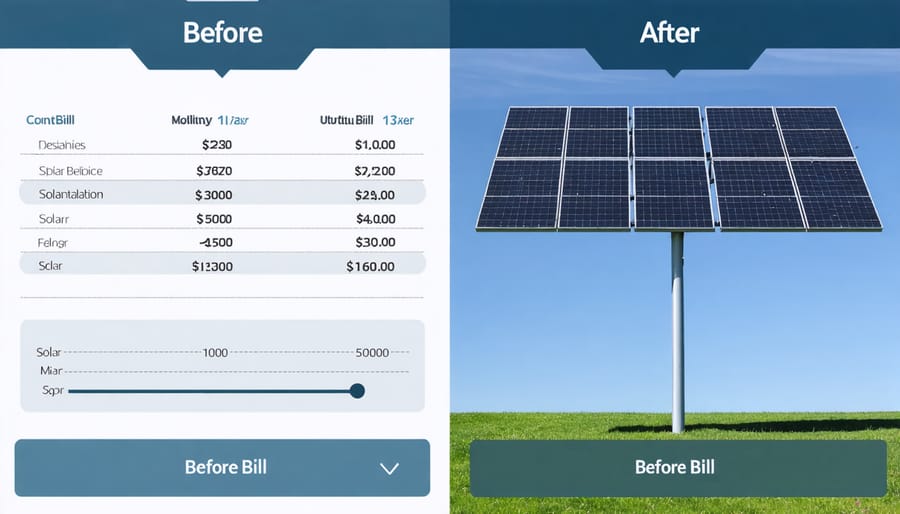

The financial benefits of zero-down solar programs become evident through comprehensive solar ROI calculations and long-term utility cost analysis. Homeowners typically experience a 20-30% reduction in their monthly electricity bills immediately after installation, with savings increasing as utility rates rise over time. These savings effectively offset the monthly solar payments, creating a cash-flow positive scenario for many households.

A detailed cost analysis reveals that over a 25-year period, the average homeowner can save between $20,000 and $30,000 on electricity costs, accounting for standard utility rate increases of 2.5-3% annually. The savings potential varies by region, with areas experiencing higher electricity rates showing more substantial returns. Solar installations also increase property values by approximately 4%, providing additional financial benefits.

The elimination of upfront costs through zero-down programs allows homeowners to realize these savings without initial capital investment. When combined with federal tax incentives, state rebates, and performance-based incentives, the long-term financial advantages become even more compelling. Most systems achieve complete payback within 7-10 years, while continuing to generate savings for decades thereafter.

Energy independence and predictable monthly payments further enhance the economic benefits, protecting homeowners from volatile energy market fluctuations and ensuring stable long-term energy costs.

Available Tax Incentives and Rebates

The federal Investment Tax Credit (ITC) remains one of the most significant incentives for solar adoption, offering a 30% tax credit on the total system cost through 2032. This substantial benefit applies to both residential and commercial installations, effectively reducing the overall investment required for solar implementation.

At the state level, incentives vary significantly but often include performance-based incentives, Solar Renewable Energy Certificates (SRECs), and property tax exemptions. California’s Net Energy Metering (NEM) program allows solar customers to receive credits for excess energy production, while New York offers the NY-Sun initiative with declining block incentives based on system size and location.

Local utilities frequently provide additional rebates and incentives to encourage solar adoption. These may include upfront rebates, performance-based incentives, or special solar-friendly rate structures. Many municipalities also offer property tax exemptions for solar installations, ensuring that the added home value from solar panels doesn’t increase property tax obligations.

Small businesses can benefit from accelerated depreciation through the Modified Accelerated Cost Recovery System (MACRS), allowing them to depreciate solar assets over five years. Additionally, some states offer specific incentives for commercial installations, including grants, low-interest loans, and tax abatements.

These incentives, combined with zero-down financing options, significantly reduce the initial barriers to solar adoption while maximizing long-term financial benefits.

Policy Framework and Support

State-Specific Programs and Regulations

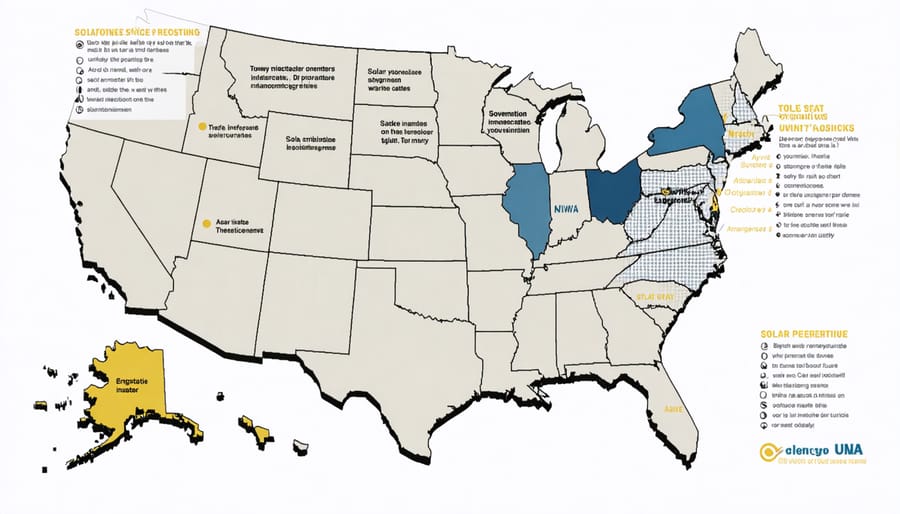

State-specific zero down solar programs vary significantly across jurisdictions, reflecting local energy policies, market conditions, and regulatory frameworks. California leads with comprehensive initiatives like the Self-Generation Incentive Program (SGIP) and net metering policies that enhance the viability of zero down installations. Massachusetts offers the SMART program, providing performance-based incentives that make zero down options more attractive to installers and consumers.

New York’s NY-Sun initiative combines with NYSERDA programs to create favorable conditions for zero down solar financing, while Arizona focuses on utility-specific programs through companies like APS and SRP. Florida’s programs primarily operate through utility partnerships and third-party financing arrangements, though with some limitations on power purchase agreements.

States like Hawaii have adapted their programs to address grid integration challenges, implementing smart export programs and time-of-use rates. Maryland and New Jersey utilize Solar Renewable Energy Credits (SRECs) alongside their zero down options, creating additional value streams for system owners. Each state’s approach reflects its unique energy landscape, solar potential, and policy objectives, requiring careful consideration when implementing zero down solar solutions.

Future Policy Trends

The landscape of zero-down solar programs continues to evolve alongside solar market trends, with several emerging policies shaping their future. The Infrastructure Investment and Jobs Act and Inflation Reduction Act have significantly expanded federal support for residential solar installations, introducing new tax incentives and grants that strengthen zero-down financing options.

State-level policies are increasingly focusing on expanding solar access to low-and-moderate-income households through innovative financing mechanisms. Many jurisdictions are implementing green banking initiatives and credit enhancement programs to reduce lender risk and improve loan terms for zero-down solar installations.

Property Assessed Clean Energy (PACE) programs are undergoing modernization, with new consumer protection measures and standardized underwriting criteria being developed. Additionally, utility companies are introducing their own zero-down solar programs in response to regulatory requirements for clean energy deployment.

These policy developments suggest a trend toward more accessible and secure solar financing options, supported by robust consumer protections and standardized industry practices. This evolution is expected to accelerate solar adoption while ensuring sustainable program growth.

Zero down solar programs have emerged as a pivotal catalyst in accelerating the widespread adoption of solar energy across residential and commercial sectors. By eliminating the substantial upfront costs traditionally associated with solar installations, these programs have successfully democratized access to renewable energy solutions. The impact extends beyond individual benefits, contributing significantly to environmental sustainability and grid resilience.

For potential adopters considering zero down solar options, it is essential to conduct thorough research and evaluation of available programs. We recommend comparing multiple providers, carefully reviewing contract terms, and understanding the long-term financial implications. Pay particular attention to interest rates, escalator clauses, and equipment warranties. Additionally, verify the installer’s credentials and track record in your local market.

The success of zero down solar initiatives demonstrates the viability of innovative financing solutions in advancing clean energy adoption. These programs have proven instrumental in helping homeowners and businesses overcome financial barriers while generating immediate energy savings. As the solar industry continues to evolve, zero down options will likely become even more refined and accessible.

Moving forward, prospective solar adopters should also consider factors such as their long-term residence plans, roof condition, and local solar incentives before committing to a program. Consulting with qualified solar professionals and financial advisors can help ensure the selected program aligns with individual circumstances and objectives. The growing availability of these financing options marks a significant step toward a more sustainable and energy-independent future.