The global solar market stands at a pivotal moment, experiencing unprecedented growth as renewable energy transitions from alternative to mainstream power generation. With installations surpassing 350 GW worldwide in 2023, the photovoltaic (PV) sector continues to reshape the energy landscape through technological innovation, declining costs, and strengthening policy support. Market dynamics reflect a complex interplay between manufacturing capacity expansion, particularly in Asia, and growing demand across both developed and emerging economies. Supply chain optimization, coupled with efficiency improvements in solar cell technology, has driven production costs down by 85% over the past decade, making solar power increasingly competitive with traditional energy sources. As governments worldwide accelerate their commitment to carbon reduction targets, the solar market emerges as a cornerstone of sustainable energy strategy, attracting substantial investment and fostering job creation across the value chain. This transformative period presents unique opportunities for stakeholders while highlighting the critical role of solar power in addressing global energy security and climate challenges.

Global Solar PV Market Overview

Market Size and Growth Projections

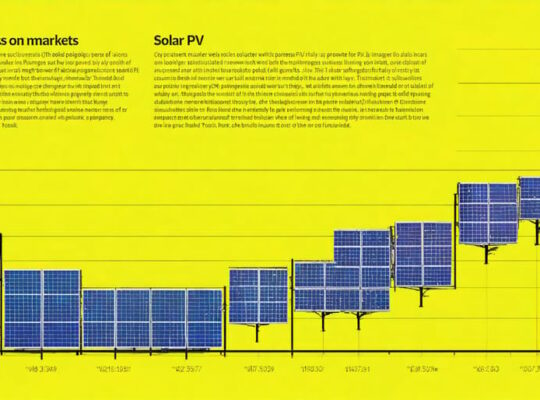

The global solar market continues to experience remarkable growth, with current valuations reaching $185.7 billion in 2023. According to industry analysts, the market is projected to achieve a compound annual growth rate (CAGR) of 20.5% through 2030, potentially reaching a valuation of $373.84 billion. This robust expansion is driven by declining technology costs, supportive government policies, and increasing corporate commitments to renewable energy adoption.

Understanding solar PV economics reveals that utility-scale installations continue to dominate market share, accounting for approximately 55% of total installations. Residential and commercial segments show strong growth trajectories, particularly in emerging markets across Asia-Pacific and Latin America.

Key growth indicators include increased manufacturing capacity, technological innovations in cell efficiency, and integration of energy storage solutions. The market demonstrates particular strength in China, the United States, and European Union countries, with developing nations rapidly accelerating their solar energy adoption rates. This expansion is further supported by the decreasing levelized cost of electricity (LCOE) for solar installations, making it increasingly competitive with traditional energy sources.

Regional Market Distribution

The global solar market exhibits distinct regional patterns, with Asia-Pacific dominating the landscape, particularly led by China’s massive deployment of photovoltaic installations. China accounts for approximately 35% of global solar capacity, followed by the European Union and North America as significant market players. Emerging markets in Latin America, particularly Brazil and Mexico, show promising growth trajectories with increasing utility-scale projects and supportive renewable energy policies.

India has emerged as a pivotal market, driven by ambitious national solar missions and decreasing installation costs. The Middle East and North Africa (MENA) region is experiencing rapid solar adoption, with the UAE and Saudi Arabia making substantial investments in utility-scale projects. Southeast Asian nations, including Vietnam and Thailand, are rapidly expanding their solar capacity through feed-in tariffs and other incentive programs.

In mature markets like Germany and Japan, the focus has shifted towards distributed generation and solar-plus-storage solutions. Australia maintains strong growth in both utility-scale and residential sectors, while African markets show potential for off-grid and mini-grid solutions, particularly in sub-Saharan regions where energy access remains a challenge.

Technology Advancements Driving Market Growth

Mono PERC Technology Evolution

Mono PERC (Passivated Emitter and Rear Cell) technology has emerged as a dominant force in the solar manufacturing landscape, marking a significant evolution in photovoltaic efficiency. This advanced cell architecture, which incorporates additional passivation and dielectric reflection layers on the rear surface, has consistently demonstrated superior performance compared to conventional solar cells.

The technology’s rapid adoption can be attributed to its ability to achieve higher conversion efficiencies while maintaining cost-effectiveness in manufacturing. Current commercial Mono PERC cells regularly achieve efficiencies exceeding 22%, with leading manufacturers pushing boundaries toward 24% in mass production.

Market penetration of Mono PERC technology has been remarkable, growing from less than 10% in 2015 to over 80% of the global solar cell production in recent years. This swift adoption has been driven by relatively minimal modifications required to existing production lines, making it an attractive upgrade for manufacturers.

Continuous improvements in PERC technology have focused on reducing light-induced degradation (LID) and light and elevated temperature-induced degradation (LeTID), which were early challenges. Advanced technologies such as gallium-doped silicon wafers and sophisticated passivation techniques have effectively addressed these issues, further cementing PERC’s position as the industry standard.

The evolution of Mono PERC has established a strong foundation for next-generation cell technologies, including TOPCon and heterojunction cells, while maintaining its cost-effectiveness and reliability advantage in current market conditions.

Emerging PV Technologies

The photovoltaic industry continues to evolve with groundbreaking innovations that enhance efficiency and expand application possibilities. Bifacial solar panels represent a significant advancement, capable of harvesting light from both sides of the panel, potentially increasing energy yield by 5-30% compared to traditional modules. These panels are particularly effective in snow-covered regions or when installed over reflective surfaces.

Another revolutionary development is the emergence of solar tiles and panels that seamlessly integrate with building architecture. These solutions address aesthetic concerns while maintaining robust energy generation capabilities, making them increasingly popular in residential applications.

Perovskite solar cells are showing promise in laboratory settings, with researchers achieving efficiency rates exceeding 29% when combined with traditional silicon cells in tandem configurations. This technology could significantly reduce manufacturing costs while improving overall system performance.

Transparent solar technologies are also gaining traction, with applications in building-integrated photovoltaics (BIPV). These innovations allow windows and other transparent surfaces to generate electricity while maintaining their primary functions, opening new possibilities for urban solar integration.

Floating solar farms represent another emerging trend, utilizing water bodies to install solar arrays. This approach not only maximizes land use efficiency but also benefits from the cooling effect of water, which can increase panel efficiency by up to 10%.

Market Trends and Competitive Landscape

Pricing Trends and Cost Analysis

The solar market has experienced significant price reductions over the past decade, with module costs declining by approximately 85% since 2010. This dramatic cost reduction, coupled with evolving solar project financing trends, has transformed the industry’s economic landscape. Current market analysis indicates that utility-scale solar installations achieve levelized cost of electricity (LCOE) values between $0.03 and $0.06 per kilowatt-hour in most regions, making solar increasingly competitive with conventional energy sources.

Manufacturing efficiency improvements, technological advances, and economies of scale continue to drive down production costs. The industry has witnessed a compound annual decrease of 20% in module prices, while balance-of-system costs have reduced by approximately 65% since 2015. These cost reductions have been particularly pronounced in major manufacturing hubs, where increased competition and automated production processes have optimized operational expenses.

Market dynamics suggest a continued downward trajectory in pricing, though at a more moderate pace than previous years. Contemporary analysis indicates that module prices may stabilize around $0.20 per watt by 2025, while total system costs could decrease by an additional 25% through improved installation efficiencies and supply chain optimization. This trend is reinforced by increasing manufacturing capacity in emerging markets and ongoing technological innovations in cell efficiency and material utilization.

The cost analysis also reveals regional variations influenced by local policies, labor costs, and market maturity. Developed markets typically demonstrate more stable pricing structures, while emerging markets show greater price volatility but often benefit from newer, more cost-effective installation technologies and methodologies.

Key Market Players and Strategies

The solar market is dominated by several key manufacturers who continually shape industry dynamics through strategic initiatives and technological innovation. Leading companies like LONGi Solar, JinkoSolar, and Trina Solar have maintained their market positions through vertical integration and economies of scale, enabling them to offer competitive pricing while maintaining product quality.

Chinese manufacturers currently control approximately 80% of global solar manufacturing capacity, leveraging advanced automation and substantial government support. However, emerging players from Europe and North America are gaining traction by focusing on premium segments and specialized applications, particularly in building-integrated photovoltaics (BIPV) and high-efficiency modules.

Market leaders are increasingly investing in research and development, particularly in n-type cell technology and heterojunction solutions. Companies like Canadian Solar and First Solar have distinguished themselves through proprietary technologies, with First Solar’s thin-film technology providing advantages in specific environmental conditions.

Strategic partnerships have become crucial, with manufacturers collaborating with energy storage providers and smart grid developers to offer comprehensive energy solutions. Many players are also expanding their presence in emerging markets through local manufacturing facilities and distribution networks.

Differentiation strategies among top manufacturers include:

– Focus on higher efficiency modules

– Enhanced warranty terms and after-sales support

– Integrated energy storage solutions

– Smart manufacturing initiatives

– Sustainable production practices

These companies are also investing in automated production lines and digital transformation to optimize operations and reduce costs, while maintaining strict quality control standards. This approach has helped maintain competitive advantages in an increasingly price-sensitive market.

Market Challenges and Opportunities

Supply Chain Considerations

The solar market’s supply chain dynamics present both challenges and opportunities for industry stakeholders. Recent global disruptions have highlighted vulnerabilities in photovoltaic component sourcing, particularly concerning raw materials like polysilicon, silver, and semiconductor materials. Manufacturing concentration in specific geographical regions has created bottlenecks, leading to price volatility and delivery uncertainties.

To address these challenges, industry leaders are implementing various strategic solutions. Vertical integration has emerged as a key strategy, with companies expanding their control across multiple supply chain segments. Additionally, manufacturers are diversifying their supplier networks and establishing regional manufacturing hubs to reduce dependency on single-source suppliers.

Supply chain digitalization and automation are revolutionizing inventory management and production planning. Advanced analytics and artificial intelligence tools enable better demand forecasting and risk assessment, while blockchain technology enhances supply chain transparency and traceability.

Sustainability considerations are increasingly shaping supply chain decisions. Companies are adopting circular economy principles, implementing recycling programs for end-of-life solar panels, and prioritizing suppliers with strong environmental credentials. This focus on sustainability not only addresses environmental concerns but also helps secure long-term supply chain resilience.

The industry is also witnessing increased collaboration between manufacturers, suppliers, and research institutions to develop alternative materials and more efficient production processes, ultimately working toward a more robust and sustainable supply chain ecosystem.

Growth Opportunities

The solar market continues to present remarkable growth opportunities driven by technological advancements, declining costs, and increasing environmental awareness. As the future of solar energy unfolds, emerging markets in Asia-Pacific and Africa are showing exceptional potential for expansion, with projected compound annual growth rates exceeding 15%.

Utility-scale solar projects are experiencing unprecedented development, particularly in regions with high solar irradiance and supportive regulatory frameworks. The integration of energy storage solutions with solar installations is creating new revenue streams and enhancing grid stability. Additionally, the commercial and industrial sectors are increasingly adopting solar power to reduce operational costs and meet sustainability goals.

Innovative financing mechanisms, including power purchase agreements (PPAs) and green bonds, are making solar installations more accessible to diverse market segments. The rise of smart grid technologies and digitalization is opening new opportunities for solar integration and grid modernization.

Building-integrated photovoltaics (BIPV) and floating solar installations represent promising market segments, especially in land-constrained regions. Furthermore, the growing adoption of electric vehicles is creating synergistic opportunities for solar charging infrastructure development, while advances in solar cell efficiency continue to improve the technology’s economic viability across different applications.

The solar market continues to demonstrate remarkable resilience and growth potential, driven by technological advancements, decreasing costs, and increasing global commitment to renewable energy adoption. Our analysis reveals that the photovoltaic sector is poised for sustained expansion, with projections indicating a compound annual growth rate of 20.5% through 2030. This growth trajectory is supported by favorable policy frameworks, improved storage solutions, and enhanced grid integration capabilities.

Key findings highlight the critical role of emerging markets, particularly in Asia-Pacific and Latin America, in shaping the future of solar energy deployment. Corporate procurement of renewable energy, coupled with innovative financing mechanisms, has emerged as a significant driver of market growth. Additionally, the integration of smart technologies and AI-driven optimization systems is revolutionizing solar asset management and operational efficiency.

Looking ahead, the solar market is expected to undergo further transformation through technological innovations, including advanced cell architectures, improved manufacturing processes, and enhanced system integration solutions. The industry’s focus on sustainability and circular economy principles will likely drive new developments in recycling and end-of-life management of solar components.

As the market matures, we anticipate increased consolidation among manufacturers, continued cost reductions, and greater emphasis on quality and reliability. These developments, combined with growing environmental awareness and supportive regulatory frameworks, position the solar market for continued expansion and evolution in the coming decades.